Carbon markets have long been hailed as a beacon of hope in the fight against climate change, touted as a mechanism to incent market participants to reduce emissions and drive investment towards more sustainable production of critical goods and services. Yet, recent revelations suggest glaring disparities between the promises of carbon markets—as currently envisioned—and their actual impact on global emissions.

Attempts to quantify the effectiveness of carbon markets have been hindered by a lack of transparency and accountability. While much of the current debate focuses on the opacity of and credit quality issues in the voluntary credit markets (“VCMs”), government issued CO2 allowance (“compliance”) markets are surprisingly opaque and have produced significant volumes of “Greenhouse Gas (GHG) permits” with little or no underlying GHG reduction value.

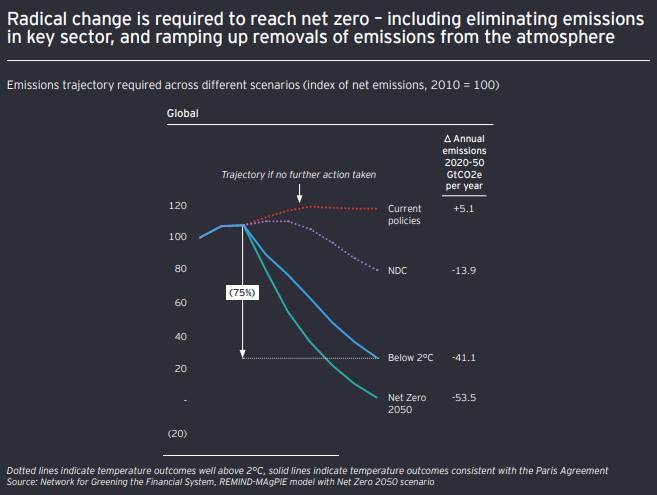

Estimates of annual man-made GHG releases to the atmosphere currently range from 53 to 57 billion (“G”) TCO2e per year. EY's "Net Zero Centre" (20220530) report says that to hold global warming to 2 degrees Centigrade, we need to cut at least 41 billion TCO2e per year, or 75% of that total by 2050. At least 15 billion per year needs to be stopped by 2030—just six years out.

The myriad of VCM and compliance markets we have launched around the world over the last 20 years, or so, have resulted in the creation of almost 36 billion CO2 credits and allowances, just over four billion of which are still in circulation. Obviously, such a significant surplus of perpetually bankable government and private registry-minted GHG discharge permits further impairs our ability to make true progress towards these daunting emission reduction goals. Some estimates suggest that in 2022, demand for VCM credits was well under 500 million TCO2e. And 60% to 70% of government-minted CO2 allowances have, so far, been handed over to the world’s largest corporate emitters, free of charge. Even if some governments keep their commitments to mint fewer free GHG discharge permits going forward, if all governments and VCM administrators proceed according to their current published plans, we could expect it to take until sometime between 2030 and 2035 for us to use up the existing (and still growing, just at a slower rate) backlog of surplus CO2 credits and allowances. There is little realistic expectation of significant emission reductions in such a future.

Credit demand projections are questionable

Many experts suggest that emitting corporations’ demand for VCM credits will be 20 to 30 times what it is today, by 2030. But such apparent demand for carbon credits and allowances is mostly driven by expected pre-purchase agreements and futures contracts that include clauses that make those future credit and allowance purchases highly conditional and speculative. The reliability of these projections is questionable, as many agreements resemble convertible debt notes and are contingent upon highly speculative future events. The intertwining of financial interests between credit suppliers, buyers and lenders further clouds the picture, casting doubt on the reliability of any demand forecasts.

When juxtaposed with the scale of emissions produced by a handful of corporations, the insignificance of the carbon market experiments we have launched, to date, becomes glaringly apparent. Meanwhile, if we account for their direct operating emissions and the GHGs that are released when their customers use the products they sell, less than 225 companies, worldwide, discharge 32 to 34 billion TCO2e/year—62% of all man-made GHGs—at the moment. Despite mounting pressure to address their environmental footprint, these companies, roughly one quarter of which are government-owned and/or controlled, continue to invest heavily in fossil fuel exploration and exploitation, and anticipate growing product end use emissions through 2035. Of course, growing their Scope 3—consumer end use--emissions undermines any progress they might achieve in reducing their operating (Scope 1) and energy use-related (Scope 2) emissions.

The reluctance of major emitters to acknowledge and address their Scope 3 emissions further underscores the inadequacy of current carbon market mechanisms. By diverting attention away from efficacious emission reduction strategies, these companies perpetuate a cycle of environmental degradation with the full support of governments that are primarily interested in establishing emissions as the sexy and politically correct new tax base. Of course, once governments get hooked on emissions-based revenues, they typically lose their enthusiasm for shrinking the basis of their new revenue stream—the emissions..

The current approach is flawed

It is evident that the current approach to carbon markets is flawed and ineffective in catalyzing meaningful change. Merely trading carbon credits and allowances without reducing atmospheric concentrations of heat-trapping gasses is a futile endeavor.

The time for complacency is over. We cannot afford to rely on half-measures and illusions of progress. It is imperative that we confront the stark reality of carbon markets and demand a paradigm shift towards genuine, impactful climate action. There is some good news. We have actually got this right before—albeit at somewhat smaller scales. We can get this right. The future of our planet depends on it.